Students can Download Tamil Nadu 11th Accountancy Previous Year Question Paper March 2019 English Medium Pdf, Tamil Nadu 11th Accountancy Model Question Papers helps you to revise the complete Tamilnadu State Board New Syllabus and score more marks in your examinations.

TN State Board 11th Accountancy Previous Year Question Paper March 2019 English Medium

General Instructions:

- The question paper comprises of four parts.

- You are to attempt all the parts. An internal choice of questions is provided wherever applicable.

- All questions of Part I, II, III, and IV are to be attempted separately.

- Question numbers 1 to 20 in Part I are Multiple Choice Questions of one mark each.

These are to be answered by choosing the most suitable answer from the given four alternatives and writing the option code and the corresponding answer. - Question numbers 21 to 30 in Part II are two-mark questions. These are to be answered in about one or two sentences.

- Question numbers 31 to 40 in Part III are three-mark questions. These are to be answered in above three to five short sentences.

- Question numbers 41 to 47 in Part IV are five-mark questions. These are to be answered in detail Draw diagrams wherever necessary.

Time: 2.30 Hours

Maximum Marks: 90

Part – I

Answer all the questions. Choose the correct answer: [20 x 1 = 20]

Question 1.

The root of financial accounting system is ______.

(a) Management accounting

(b) Responsibility accounting

(c) Social accounting

(d) Stewardship accounting

Answer:

(d) Stewardship accounting

Question 2.

The business is liable to the proprietor of the business in respect of capital introduced by the person according to _________.

(a) Business entity concept

(b) Dual aspect concept

(c) Money measurement concept

(d) Cost concept

Answer:

(a) Business entity concept

Question 3.

A firm has assets of ₹ 1,00,000 and the external liabilities of ₹ 60,000. Its capital would be _______.

(a) ₹ 1,00,000

(b) ₹ 40,000

(c) ₹ 1,60,000

(d) ₹ 60,000

Answer:

(b) ₹ 40,000

Question 4.

The amount brought into the business by the proprietor should be credited to ________.

(a) Capital Account

(b) Suspense Account

(c) Cash Account

(d) Drawings Account

Answer:

(a) Capital Account

![]()

Question 5.

The difference of totals of both debit and credit side of trial balance is transferred to _______.

(a) Suspense Account

(b) Miscellaneous account

(c) Trading account

(d) Difference account

Answer:

(a) Suspense Account

Question 6.

The Cash book records _______.

(a) All cash payments

(b) All credit transactions

(c) All cash receipts and cash payments

(d) All cash receipts

Answer:

(c) All cash receipts and cash payments

Question 7.

A bank reconciliation statement is prepared with the help of ________.

(a) Bank statement and bank column of the cash book

(b) Petty cash book

(c) Bank statement

(d) Cash book

Answer:

(a) Bank statement and bank column of the cash book

Question 8.

Errors of principle arises when:

(a) Distinction is not made between capital and revenue items

(b) There are wrong postings and wrong castings

(c) There is complete omission of a transaction

(d) There is partial omission of a transaction

Answer:

(a) Distinction is not made between capital and revenue items

Question 9.

The following error becomes unavoidable in computerised accounting:

(a) Error of partial omission

(b) Error in carrying forward

(c) Casting error

(d) Error of duplication

Answer:

(d) Error of duplication

Question 10.

Residual value of an asset means the amount that it can fetch on sale at the _______ of its useful life.

(a) Middle

(b) Beginning

(c) End

(d) None of these

Answer:

(c) End

Question 11.

Expenditure incurred ₹ 20,000 for trial run of a newly installed machinery will be _________.

(a) Capital Expenditure

(b) Deferred Revenue Expenditure

(c) Preliminary Expenditure

(d) Revenue Expenditure

Answer:

(a) Capital Expenditure

Question 12.

Huge amount spent on advertisement by Mr.Ravi for his business promotion is ________.

(a) Revenue Receipts

(b) Deferred Revenue Expenditure

(c) Capital Expenditure

(d) Revenue Expenditure

Answer:

(b) Deferred Revenue Expenditure

![]()

Question 13.

Choose the correct pair:

(i) Capital Expenditure – It increases the profit earning capacity of the business

(ii) Revenue Expenditure – To get benefit for certain years

(iii) Deferred revenue expenditure – It is recurring in nature

(a) (iii) correct

(b) (i),(ii),(iii) all are correct

(c) (i) correct

(d) (ii) correct

Answer:

(c) (i) correct

Question 14.

Balance sheet shows the _______ of the business.

(a) Financial position

(b) Purchases

(c) Profitability

(d) Sales

Answer:

(a) Financial position

Question 15.

Net profit is ________.

(a) Debited to Drawing A/c

(b) Credited to Drawing A/c

(c) Debited to Capital A/c

(d) Credited to Capital A/c

Answer:

(d) Credited to Capital A/c

Question 16.

Which one is not a component of computer system?

(a) Data

(b) Central processing unit

(c) Input unit

(d) Output unit

Answer:

(a) Data

Question 17.

An example of output device is ________.

(a) Mouse

(b) Keyboard

(c) Optical scanner

(d) Printer

Answer:

(d) Printer

Question 18.

Tally is an example of:

(a) Inbuilt accounting system

(b) Readymade accounting software

(c) Tailor made accounting software

(d) Customised accounting software

Answer:

(b) Readymade accounting software

Question 19.

The source document or voucher used for recording entries in sales book is ________.

(a) Invoice

(b) Cash receipt

(c) Debit note

(d) Credit note

Answer:

(a) Invoice

![]()

Question 20.

Purchases of fixed assets on credit basis is recorded in ________.

(a) Purchase return book

(b) Journal proper

(c) Purchase book

(d) Sales book

Answer:

(b) Journal proper

Part – II

Answer any seven questions in which question No. 30 is compulsory: [7 x 2 = 14]

Question 21.

List any two functions of accounting.

Answer:

The main functions of accounting:

- Measurement

- Forecasting

1. Measurement: The main function of accounting is to keep, systematic record of transactions, post them in the ledger and ultimately prepare the final accounts.

2. Forecasting: With the help of the various tools of accounting, future performance and financial position of the business enterprises can be forecasted.

Question 22.

Define book-keeping.

Answer:

“Book-keeping is an art of recording business dealings in a set of books”. – J.R.Batlibai. “Book-keeping is the science and art of recording correctly in the books of account all those business transactions of money or money’s worth”. – R.N.Carter.

Question 23.

Give the golden rules of double entry accounting system.

Answer:

The consistency convention implies that

| Personal account | Debit the receiver | Credit the giver |

| Real account | Debit what comes in | Credits what goes out |

| Nominal account | Debit all expenses and losses | Credit all incomes and gains |

![]()

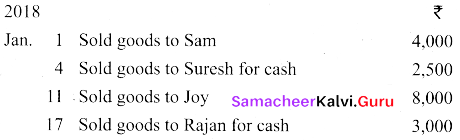

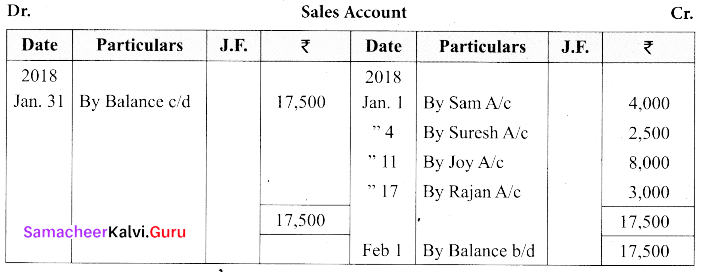

Question 24.

Prepare a Sales account from the following transactions.

Answer:

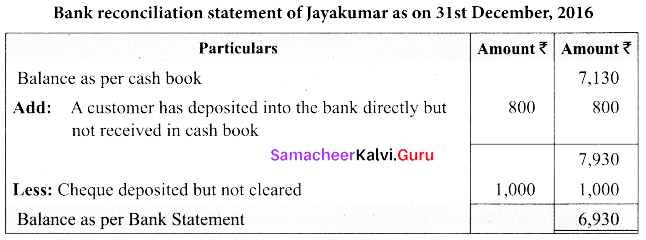

Question 25.

From the following particulars prepare a bank Reconciliation Statement of Mr. Kumar as on 31.12.2016.

(a) Balance as per cash book ₹ 7,130

(b) Cheque deposited but not cleared ₹ 1,000

(c) A customer has deposited ₹ 800 into the hank directly

Answer:

Question 26.

What are compensating errors?

Answer:

The errors that make up for each other or neutralize each other are known as compensating errors. These errors may occur in related or unrelated accounts. Thus, excess debit or credit in one account may be compensated by excess credit or debit in some other account. These are also known as offsetting errors.

![]()

Question 27.

Calculate the amount of depreciation under Straight Line Method.

Cost of the Asset ₹ 1,00,000

Estimated Residual Value ₹ 5,000

Expected useful life 5 years.

Answer:

Question 28.

Name any two direct expenses.

Answer:

Direct expenses:

- Carriage inwards or freight inwards

- Wages

Question 29.

What are adjusting entries?

Answer:

Adjustment entries are the journal entries made at the end of the accounting period to account for items which are omitted in trial balance and to make adjustments for outstanding and prepaid expenses and revenues accrued and received in advance.

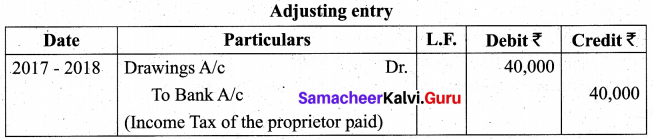

Question 30.

Mr. Babu, a sole proprietor whose Income Tax for the year 2017 – 2018 ₹ 40,000 is paid by the business. Give adjusting entry.

Answer:

Part – III

Answer any seven questions in which question No. 40 is compulsory: [7 x 3 = 21]

Question 31.

Enumerate the importance of accounting.

Answer:

The importance of accounting is:

- Systematic records: All the transactions of an enterprise which are financial in nature are recorded in a systematic way in the books of accounts.

- Preparation of financial statements: Results of business operations and the financial position of the concern can be ascertained from accounting periodically through the preparation of financial statements.

- Assessment of progress: Analysis and interpretation of financial data can be done to assess the progress made in different areas and to identify the areas of weaknesses.

![]()

Question 32.

Write short notes on:

(i) Business Entity Concept

(ii) Going Concern Concept

Answer:

(i) Business Entity Concept

This concept implies that a business unit is separate and distinct from the owner or owners, that is, the persons who supply capital to it. Based on this concept, accounts are prepared from the point of view of the business and not from the owner’s point of view. Hence, the business is liable to the owner for the capital contributed by him/her.

(ii) Going Concern Concept

It is the basic assumption that business is a going concern and will continue its operations for a foreseeable future. Going concern concept influences accounting practices in relation to valuation of assets and liabilities, depreciation of the fixed assets, treatment of outstanding and prepaid expenses and accrued and unearned revenues.

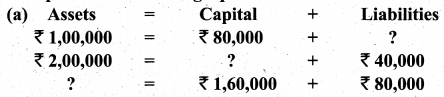

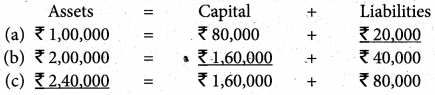

Question 33.

Complete the accounting equation

Answer:

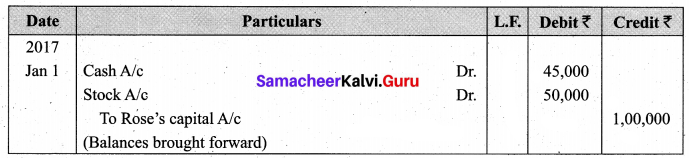

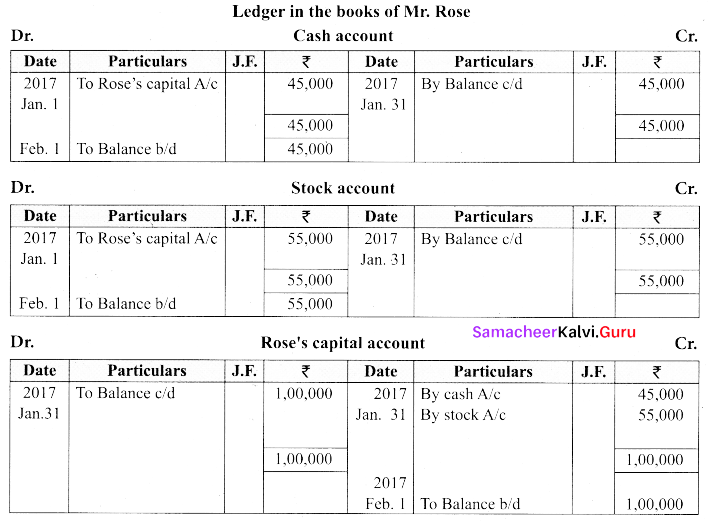

Question 34.

Prepare necessary Ledger accounts in the books of Mr. Rose from the following opening entry.

Answer:

![]()

Question 35.

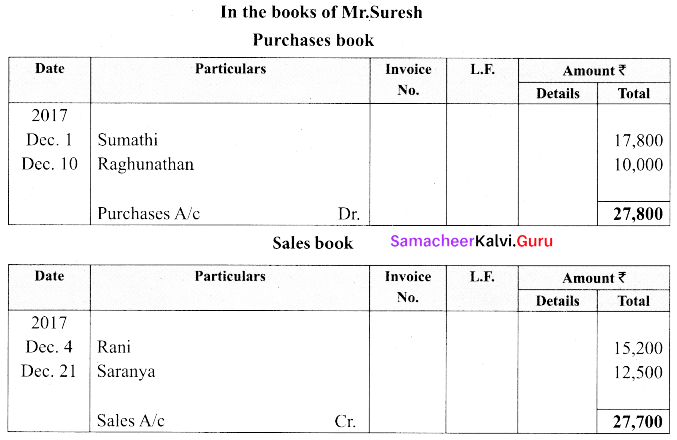

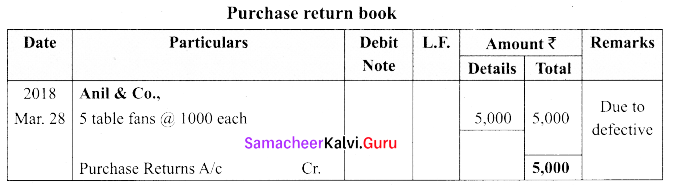

Enter the following transactions in the purchases and sales books of Mr. Suresh, an automobile dealer, for the month of December, 2017.

| 2017 | ₹ | |

| Dec. 1 | Bought from Sumathi on credit | 17,800 |

| Dec. 4 | Sold goods to Rani on credit | 15,200 |

| Dec. 10 | Purchased goods on credit from Raghunathan | 10,000 |

| Dec. 21 | Sold goods on credit to Saranya | 12,500 |

| Dec. 26 | Sold goods to Shyam for cash | 3,000 |

Answer:

Question 36.

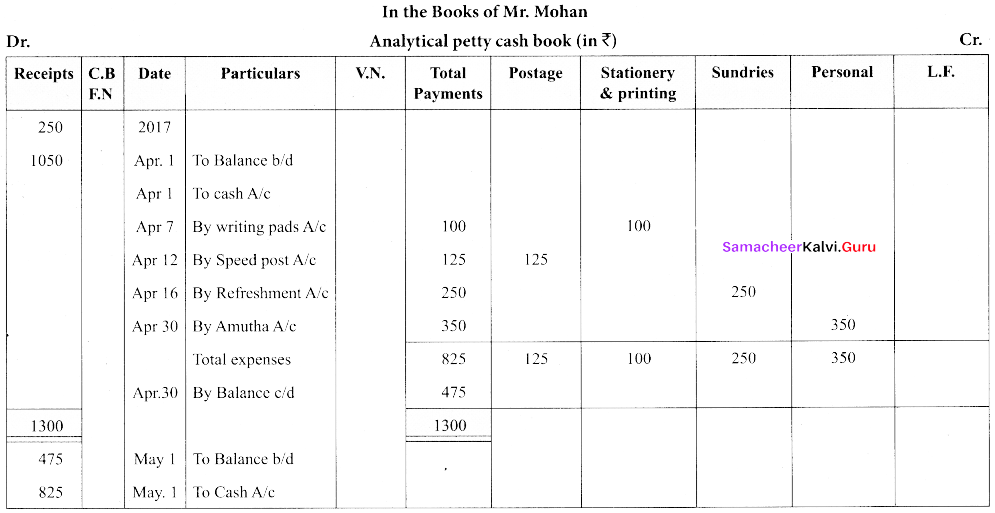

Prepare an analytical petty cash book of Mr. Mohan from the following particulars under imprest system:

2017 | ₹ | |

| April. 1 | Balance on hand | 250 |

| April. 1 | Cash received from chief cashier | 1,050 |

| April. 7 | Paid for writing pads and registers | 100 |

| April. 12 | Paid for speed post | 125 |

| April. 16 | Refreshment expenses | 250 |

| April. 30 | Paid to Amutha on account | 350 |

Answer:

![]()

Question 37.

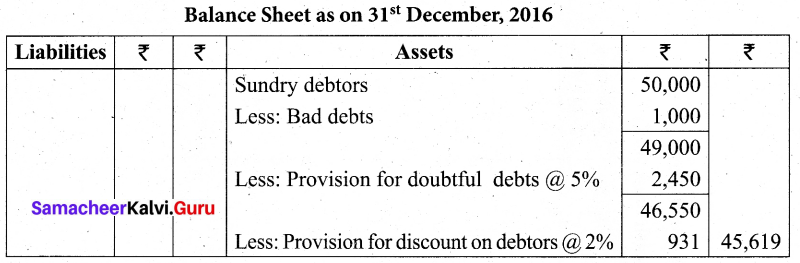

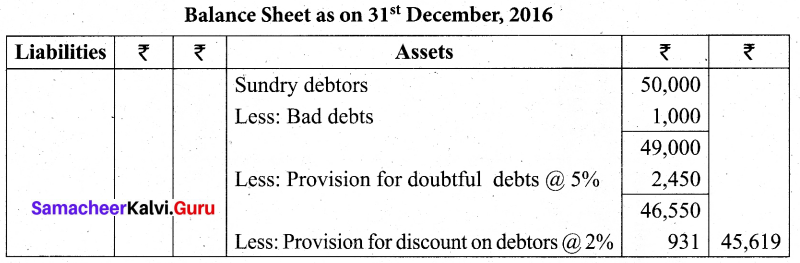

The trial balance of a trader on 31st December, 2016 shows sundry debtors as ₹ 50,000. Adjustments:

(a) Write off ₹ 1,000 as bad debts

(b) Provide 5% for doubtful debts

(c) Provide 2% for discount on debtors

Show how these items will appear in the profit and loss A/c and balance sheet of the trader.

Answer:

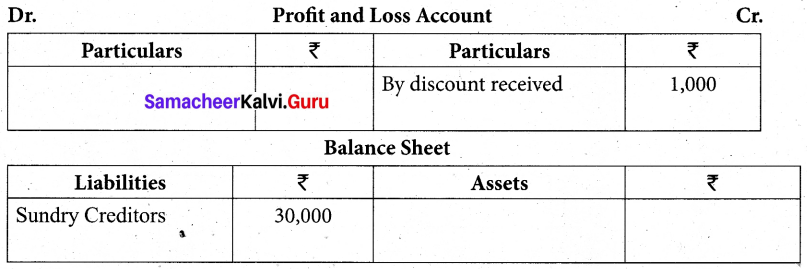

Question 38.

The following are the extracts from the trial balance:

| Particulars | Debit ₹ | Credit ₹ |

| Sundry Creditors | 30,000 | |

| Discount received | 1,000 |

Answer:

Question 39.

Write short notes on:

(i) Hardware

(ii) Software

Answer:

(i) Hardware: The physical components of a computer constitute its hardware. Hardware . consists of input devices and output devices that make a complete computer system.

(ii) Software: A set of programs that form an interface between the hardware and the user of a computer system are referred to as software.

![]()

Question 40.

A textile business unit sells some part of its unused land and received the amount.

(i) Can it be considered as normal sale?

(ii) State whether the transaction is of capital or revenue nature and explain.

Answer:

(i) No, it cannot be considered as normal sale because this is capital receipts for that business.

(ii) The transaction is capital receipt because he does a textile business. These some part of its unused land sold and he received the amount for that land. So this is not considered as normal sale.

Part – IV

Answer all the questions: [7 x 5 = 35]

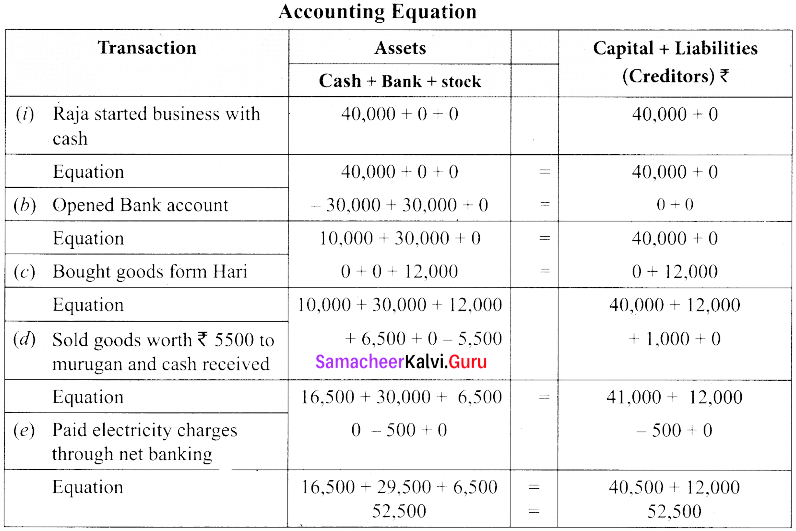

Question 41.

(a) For the following transactions, show the effect on accounting equation.

(i) Raja started business with cash – ₹ 40,000

(ii) Opened bank account with a deposit of – ₹ 30,000

(iii) Bought goods from Hari on credit for – ₹ 12,000

(iv) Sold goods worth ₹ 5,500 to Murugan and cash received – ₹ 16,500

(v) Paid electricity charges through net banking – ₹ 500

Answer:

[OR]

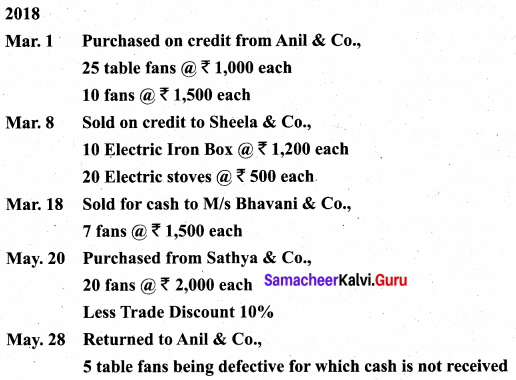

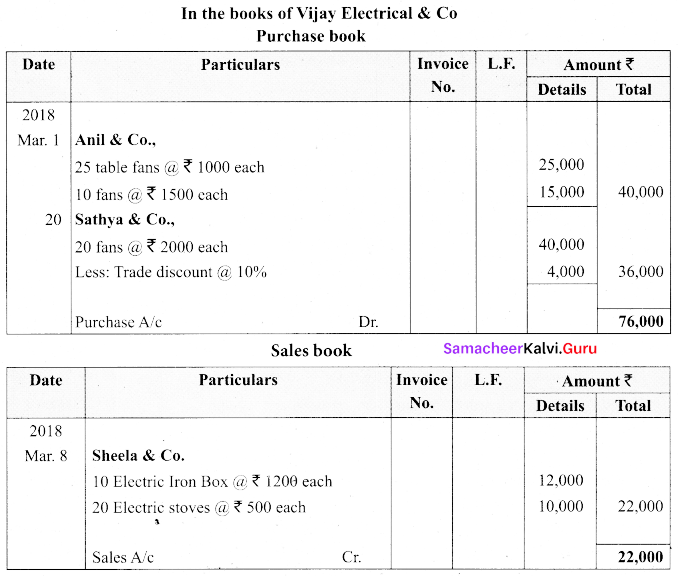

(b) Record the following transactions of Vijay Electrical & Co, in its subsidiary books.

Answer:

Note: March 18, Cash transaction so it can not be taken into account.

![]()

Question 42.

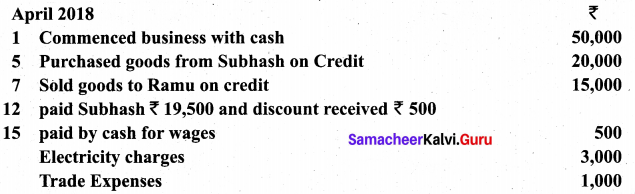

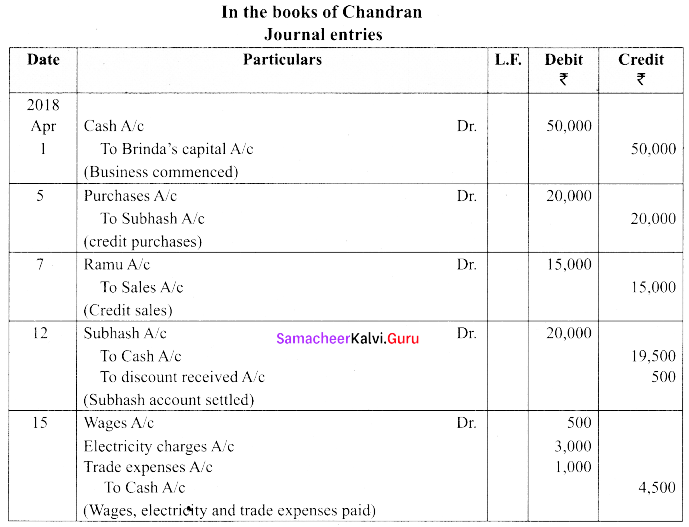

(a) Pass Journal entries in the books of Brinda who is a dealer in sport materials.

Answer:

[OR]

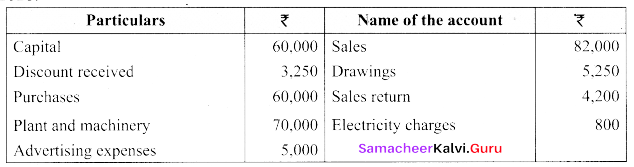

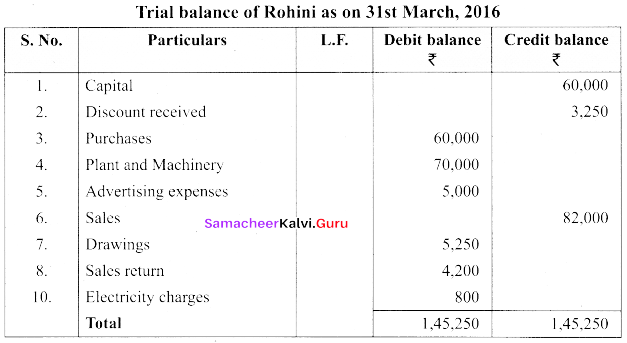

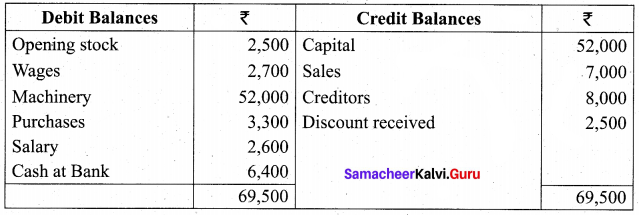

(b) From the following balances of Rohini, prepare the trial balance as on 31st March, 2018.

Answer:

Question 43.

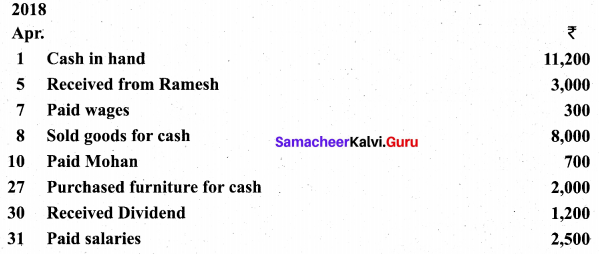

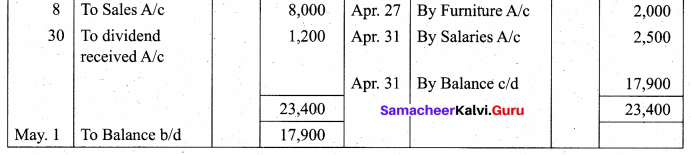

(a) Enter the following transactions in a simple cash book of Kunal:

Answer:

[OR]

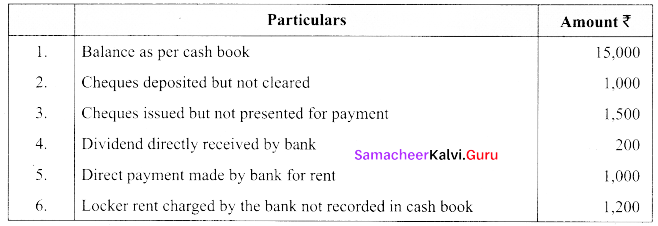

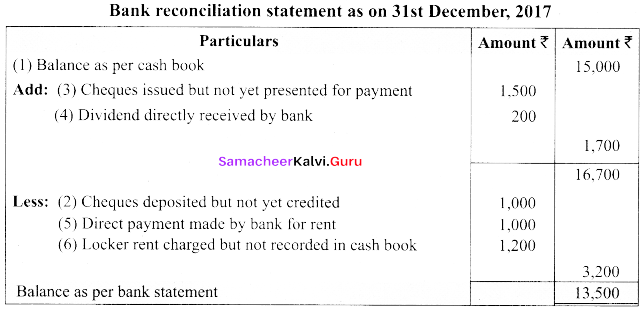

(b) From the following information, prepare bank reconciliation statement to find out the bank statement balance as on 31st December, 2017.

Answer:

![]()

Question 44.

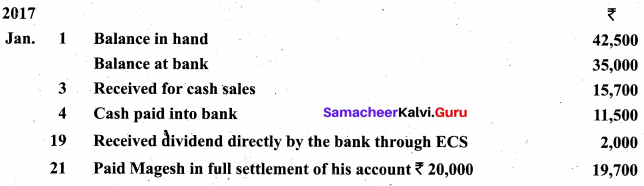

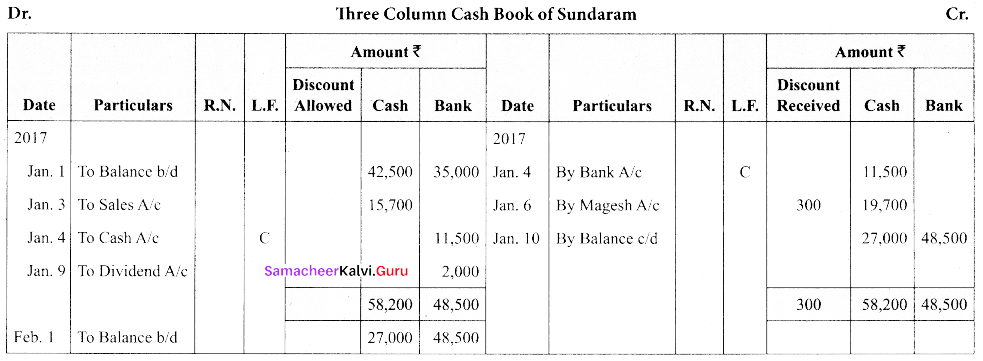

(a) Enter the following transactions in the three column cash book of Sundaram

Answer:

[OR]

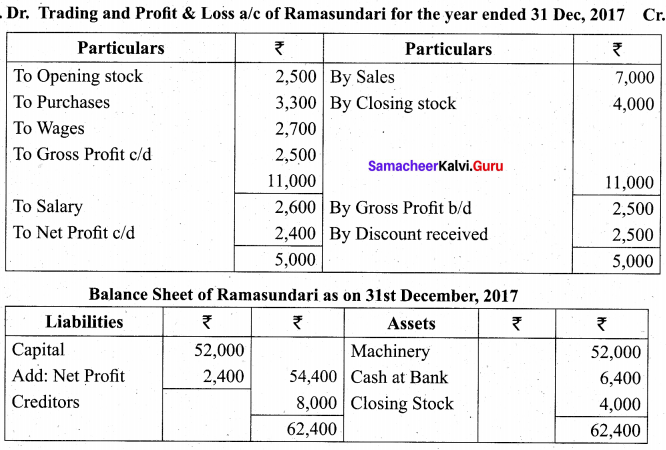

(b) Prepare trading and profit and loss account in the books of Smt. Ramasundari for the year ended 31st December, 2017 and balance sheet as on that date from the following information:

Answer:

Question 45.

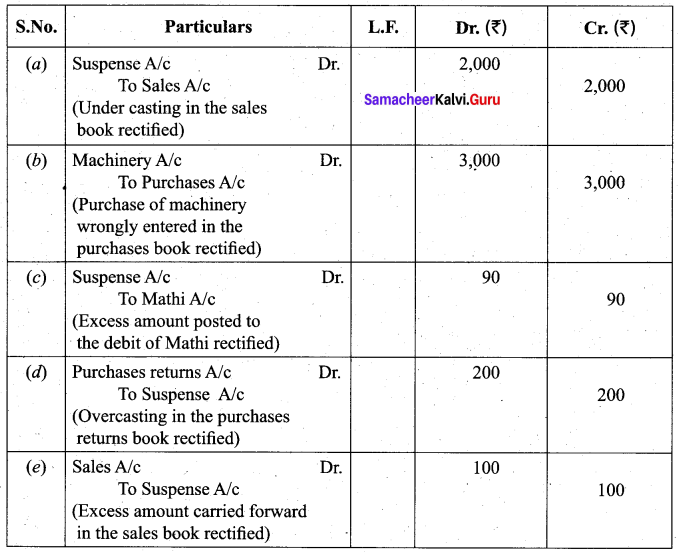

(a) Pass journal entries to rectify the following errors located after the preparation of the trial balance. Assume that there exists a suspense account.

(a) The total of sales book was undercast by ₹ 2,000.

(b) The purchase of machinery for ₹ 3,000 was entered in the purchases book.

(c) A credit sale of goods for ₹ 450 to Mathi was posted in his account as ₹ 540.

(d) The purchases returns book was overcast by ₹ 200.

(e) The total of sales book ₹ 1,122 were wrongly posted in the ledger as ₹ 1,222.

Answer:

[OR]

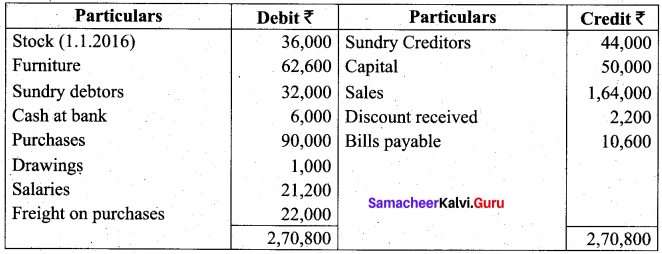

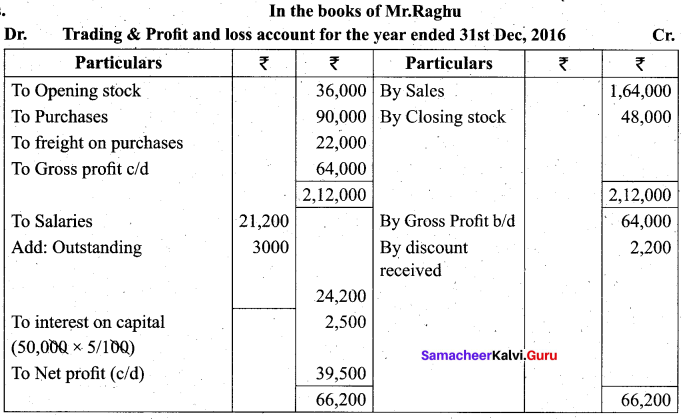

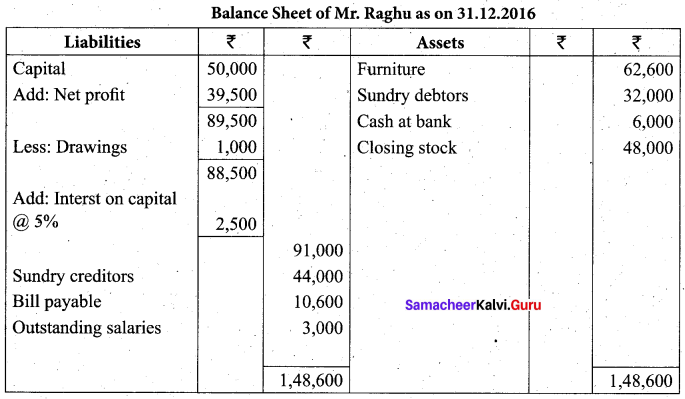

(b) From the following Trial balance of Mr. Raghu, prepare his trading and profit and loss A/c and the balance sheet as 31.12.2016.

Following adjustments are to be made:

(a) Outstanding salaries ₹ 3,000

(b) Closing stock; was valued at ₹ 48,000

(c) Provide, for 5% interest on Capital

Answer:

![]()

Question 46.

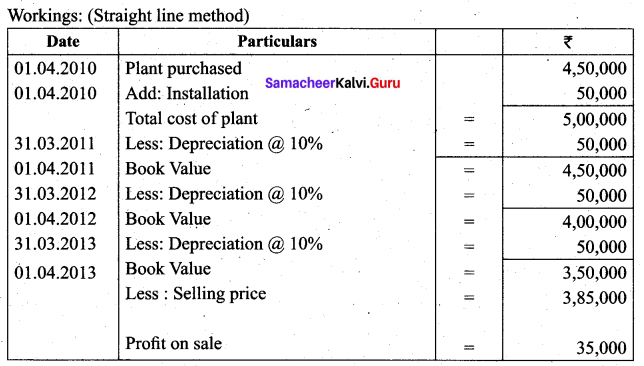

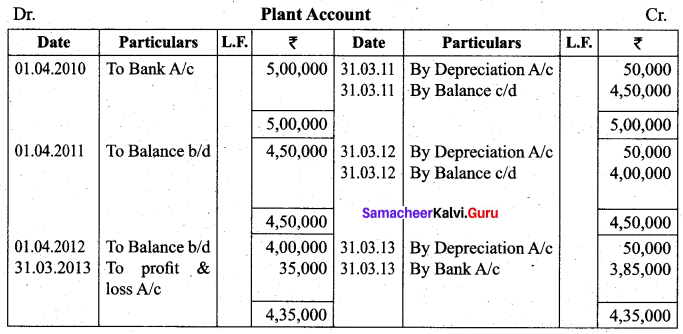

(a) Sudha manufacturing Company purchased on 1 April 2010, a plant for ₹ 4,50,000 and spent ₹ 50,000 on its installation. After having used it for three years, it was sold for ₹ 3,85,000. Depreciation is to provided every year at the rate of 10% per annum straight line method. Accounts are closed on 31st March every year. Show machinery account.

Answer:

[OR]

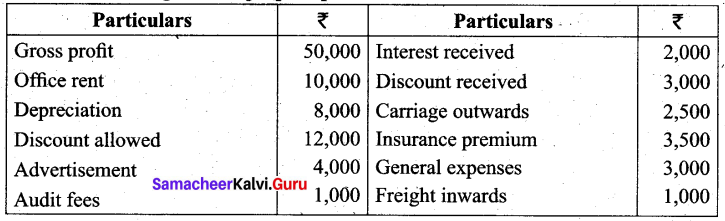

(b) From the following details, prepare profit and loss account.

Answer:

![]()

Question 47.

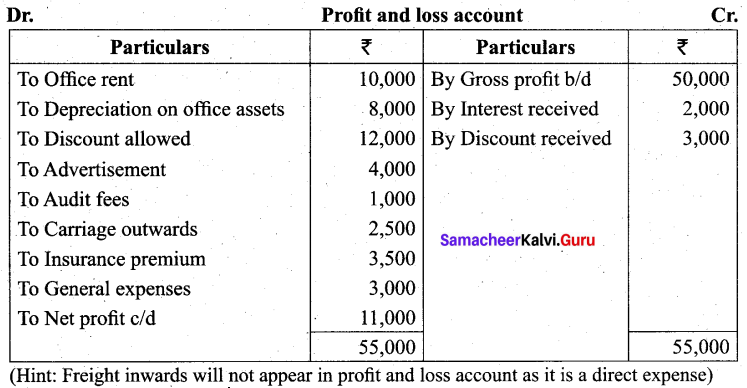

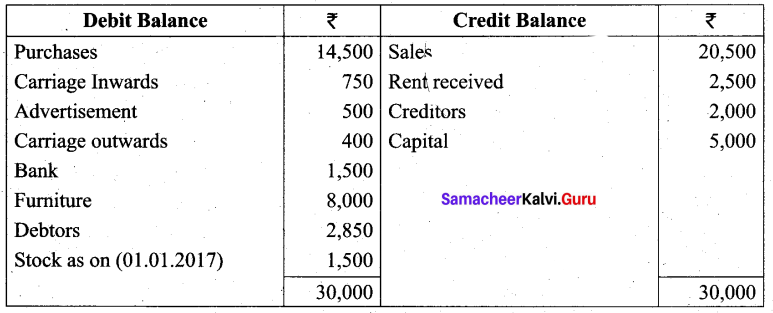

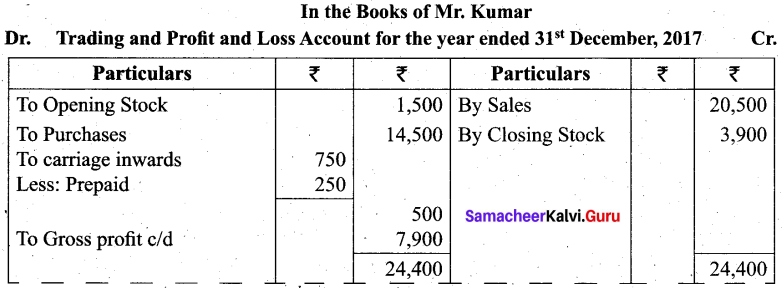

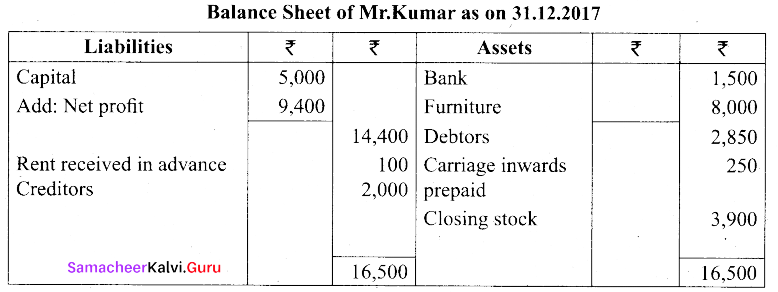

(a) From the following information, prepare Trading & Profit & Loss A/c and Balance sheet of Mr. Kumar for the year ending 31st December, 2017.

Adjustments:

(a) Closing stock was valued at ₹ 3,900

(b) Carriage inwards prepaid ₹ 250

(c) Rent received in advance ₹ 100

Answer:

[OR]

(b) Explain the three methods of codification with examples.

Answer:

Methods of codification :

(a) Sequential codes:

In sequential code, numbers and/or letters are assigned in consecutive order. These codes are applied primarily to source documents such as cheques, invoices, etc. A sequential code can facilitate document search. For example:

| Code | Accounts |

| CL001 | ABC LTD |

| CL002 | XYZ LTD |

| CL003 | SCERT |

(b) Block codes:

In a block code, a range of numbers is partitioned into a desired number of sub-ranges and each sub-range is allotted to a specific group. In most of the cases of block codes, numbers within a sub-range follow sequential coding scheme, i.e., the numbers increase consecutively. For example:

| Code | Dealer type |

| 100 – 199 | Small pumps |

| 200 – 299 | Medium pumps |

| 300 – 399 | Pipes |

| 400 – 499 | Motors |

(c) Mnemonic codes

A mnemonic code consists of alphabets or abbreviations as symbols to codify a piece of information. For example:

| Code | Information |

| SJ | Sales Journals |

| HQ | Head Quarter |